Usually people, who are new to the concept of financial models, have a misconception that there is only one type of financial model which is a three statement model (including Statement of Profit & Loss, Balance Sheet, Cash Flow Statement).

Understanding what is financial modelling and the various types of financial models, different purposes is very important who are planning a career in the field of Finance. We will be discussing about the most relevant Financial Models in 2023 through this article.

[lwptoc]

TYPES OF FINANCIAL MODELS

- Three Statement Model

- Credit Rating Model

- Discounted Cash Flow (DCF) Model

- Comparable Analysis Model

- Merger Model

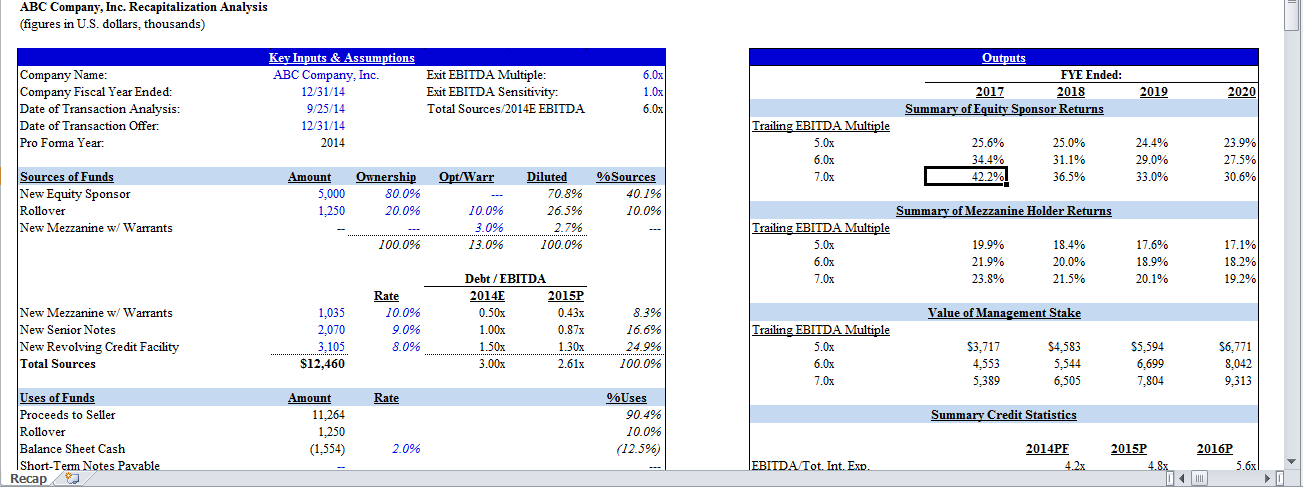

- Leveraged Buyout (LBO) Model

- Model with Scenarios

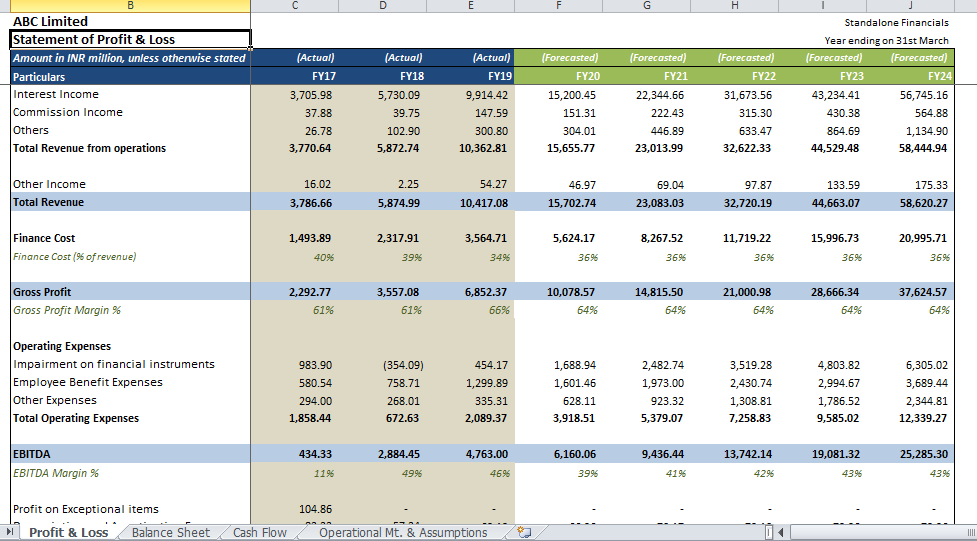

THREE STATEMENT MODEL

This is the very basic kind of model which only includes three financial statements (Statement of Profit & Loss, Balance Sheet and Cash Flow Statement), as suggested by the name. It requires one to make certain assumptions and only work on the future projections of these 3 statements. There are subsequent schedules which are required to be prepared which will support the statements including:

- Depreciation Schedule

- Fixed Assets Schedule

- Working Capital Schedule

- Debt Schedule

- Tax Schedule etc.

CREDIT RATING MODEL

Credit rating Model is usually prepared by the Banks, NBFCs or other Financial Institutions for the purpose of assessing credit worthiness of the borrower. It is only prepared for the purpose of extending debt funding to the borrower.

It involves working on various ratios including liquidity (like DSCR), Profitability (Interest Coverage Ratio, Profit Margins), Solvency (Debt Equity Ratio, Total Liabilities to Equity Ratio etc.) Credit Rating Model stresses upon the structure of interest payments and principal repayments by the borrower in a timely manner.

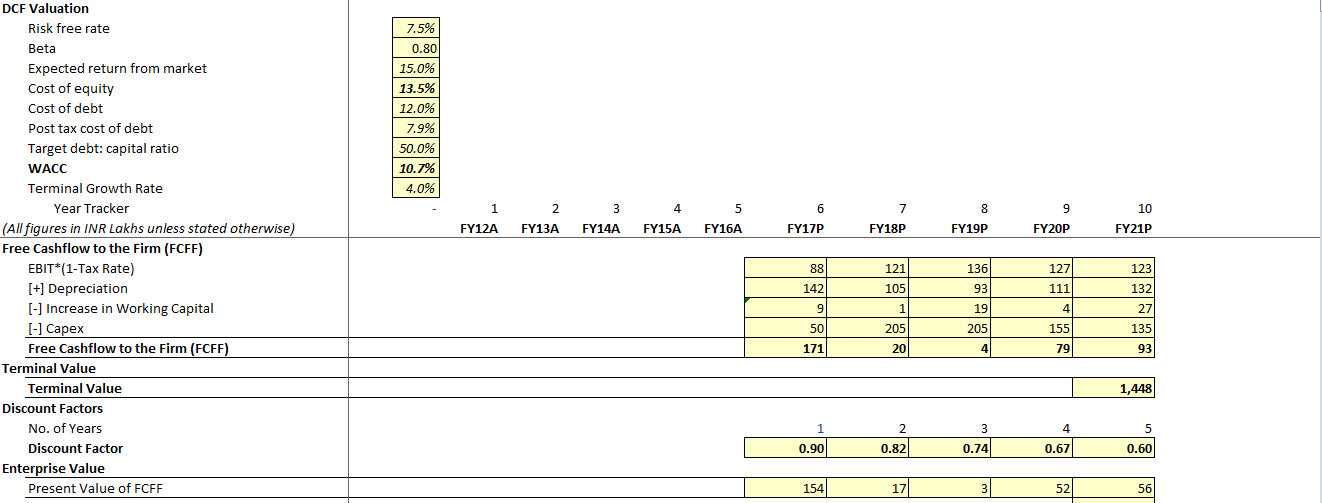

DISCOUNTED CASH FLOW (DCF) MODEL

DCF Model is another prominent type of model which is prepared by Investment Bankers, Management Consultants, Private Equity or Venture Capital people to conduct valuation through cash flows of the company.

They are two types of valuations- Absolute Valuation and Relative Valuation. Absolute Valuation consists of valuation performed through DCF, Dividend Distribution Method etc. Relative Valuation consists of valuation conducted through Trading and Transaction Comparable.

Valuation using DCF method is usually prepared in DCF model. It is an addition of three statement model with valuation calculation which is an extension from the forecasted cash flows.

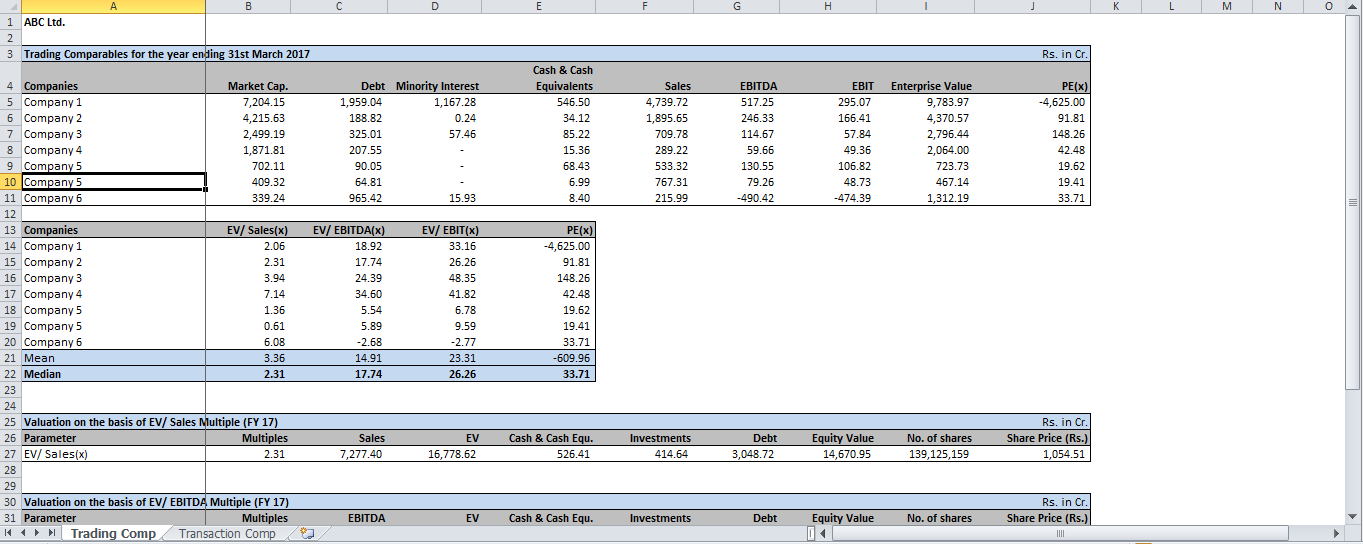

COMPARABLE ANALYSIS MODEL

Comparable Analysis Model is very similar to DCF Model. It is also a composite of three statement model and the valuation. However, the only difference in Comparable Analysis model is that it is made through comparable analysis valuation or valuation multiples using trading and transaction comparable.

Trading comparable is performed through assessing the valuation multiples of similar companies listed in the stock exchanges and transaction comparable is performed through evaluating the fund raising or M&A transactions of similar companies happened in the past.

MERGER MODEL

Merger Model, as the name suggests, is prepared specifically in case of merger or acquisition of the target by the acquirer. This is a unique type of model which captures the financials and financial performance of both the companies (Target and the Acquirer) with the adjustments of their synergies.

Typically, there are three steps to prepare a merger model as listed below:

- Preparing a separate model of the acquirer with future projections

- Preparing a separate model of the target with future projections

- Merging both the models into keeping some of the adjustments for the synergies which both the companies will bring to each other’s business.

LEVERAGED BUYOUT (LBO) MODEL

Leverage Buyout is a situation in which the acquirer buys a target company using very small portion of his own capital and a major portion of debt or non-equity source which is raised from the market (Banks, NBFCs, Financial Institutions etc.). Assets of the both the companies usually become the collateral of the loan in this situation.

The model is built keeping in mind both the situations:

- Acquisition of the target company

- Raising loan from the market through collateralizing assets of the companies

Major characteristic of a leveraged buyout model is that it only considers debt or non-equity source (like, mezzanine debt, subordinate debt etc.) as a source of external capital in order to earn highest return from the investment as debt is the cheapest source currently which is available in the market.

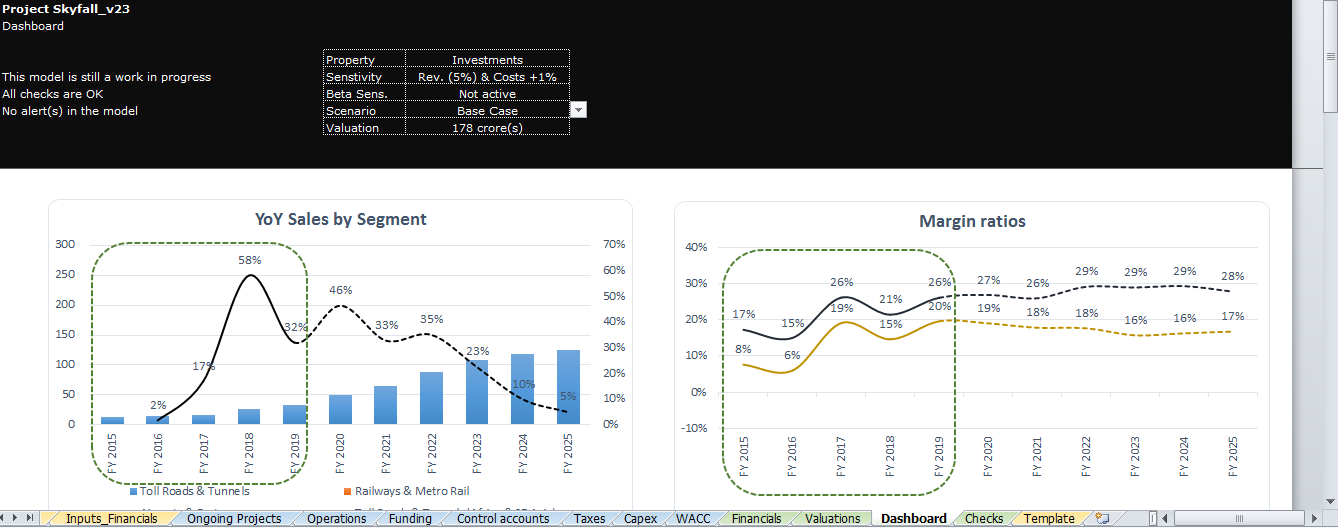

MODEL WITH SCENARIOS (CONVERTIBLE MODEL)

This is a unique type of model which is prepared by high skilled financial analysts. They link the whole model in such a manner that one can see different projections of different scenarios in just one model. The same model shows different results when one changes the scenarios from the assumption sheet.

Usually model with scenarios are prepared keeping three situations in mind:

- Optimistic (Management)

- Actual (Base)

- Pessimistic (Conservative or Investor)