One of the most persistent dilemmas that companies and businesses face these days is which project to invest in and how the resources must be allocated. Capital budgeting techniques can be used to assess the value of such investments and determine which one will have the highest impact on the company value as well as maximise shareholders’ wealth.

What is Capital Budgeting?

Capital budget is the process of determining and evaluating long-term investments that contribute toward wealth maximisation of shareholders. In other words, capital budgeting helps in deciding whether to accept or reject a project and will the investment be fruitful in future years.

Key Highlights:

- Contributes to decision making related to investment opportunities.

- Helps in the understanding of the effects of the investments on businesses and the risks involved in it.

- Widely used techniques of Capital Budgeting are:

- Net Present Value (NPV)

- Internal Rate of Return (IRR)

- Payback Period and Discounted Payback Method

Components in Capital Budgeting

There a mainly three aspects when it comes to capital budgeting fundamentals and the capital budgeting process:

- How much of initial investment is required?

Initial Investment = Cost of Fixed Assets + Installation Expenses – Sale of Old Assets + Tax on Capital Gain – Tax Savings on Capital Loss + Additional Working Capital

- What will be the annual cash inflows?

Method 1: Subsequent Cash Inflows = Sale – Variable Expenses – Fixed Expenses – Depreciation – Tax + Depreciation – Capital Expenditure

Method 2: Subsequent Cash Inflows = Net Profit + Depreciation + Interest (1- Tax Rate) – Capital Expenditure

- What is the terminal cash flow from the project? Or what is the residual value of the asset?

Terminal Cash Flow = Scrap of New Asset – Tax on Capital Gain + Tax Savings on Capital Loss + Working Capital

Main Capital Budgeting Evaluation Techniques: NPV, IRR, Payback – Using Excel Examples

Capital budgeting has been a crucial part of financial modelling and is used to determine the value of projects in the coming years. We will understand some main techniques and their limitations along with examples when it comes to financial project evaluation.

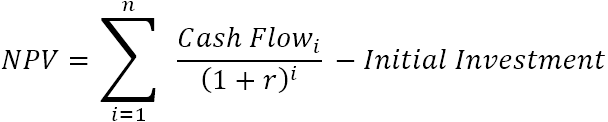

- Net Present Value (NPV):

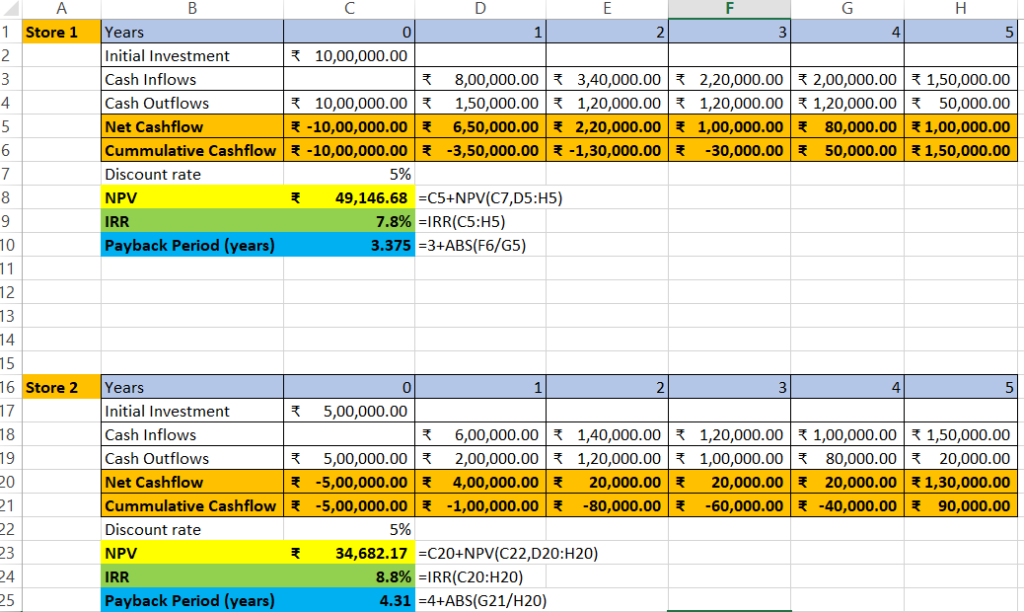

This is a form of Discounted Cash Flow (DCF) technique, which can be derived by summation of present values of cash proceeds in each year minus the summation of present values of net cash outflows in each year.

In formula, it can be represented as:

However, it can be tiring to use such lengthy formulas manually. That’s where Excel comes to rescue. Microsoft Excel has an embedded formula for NPV to make our task easier.

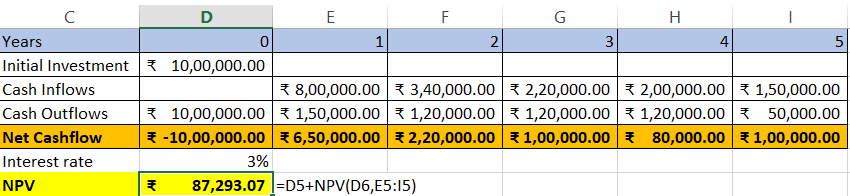

Let’s take a look at an example:

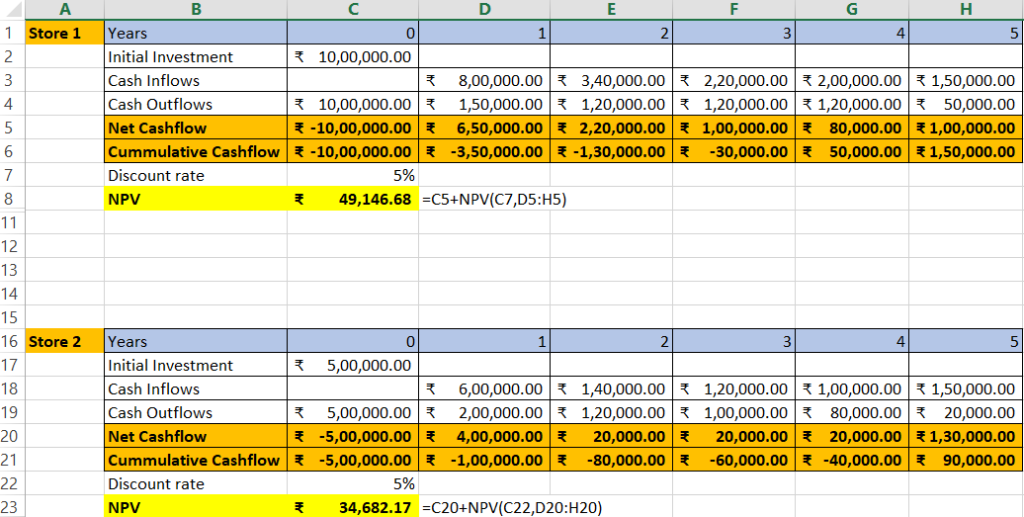

Suppose you are working in the financial planning and analysis department of DMart and they are planning to open two new stores. The management would like to know if this is financially possible or not. Here we will implement the NPV method to evaluate the viability:

# Net Cash Flow is Cash Inflow minus Cash Outflow.

# While computing NPV, we start from year 1 rather than year 0 and later add the initial investment.

The general rule while making a decision about the project using NPV is if:

- NPV > zero, accept the project.

- NPV < zero, reject the project.

- In case of multiple projects and limited resources, projects will be ranked according to NPV and the highest one will be prioritised.

NPV is not free from limitations:

- It does not account for project size comparison. Initial investment in both the stores are significantly different, so the NPV would not justify the scale very well.

- The discount or interest rate assumption also affects the NPV significantly.

At 5% and 3% interest rate, NPV changes by almost Rs. 38,147.

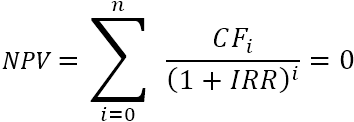

- Internal Rate of Return (IRR)

The second DCF technique is the Internal Rate of Return. It is also known as yield on investment, marginal efficiency of capital, marginal productivity of capital, rate of return and so on. IRR is the rate of return that a project earns. In other words, IRR is the discount rate that equates the PV of the cash inflows to the initial investment and causes NPV to become zero.

Mathematically, IRR can be expressed as:

Let’s continue with our previous example:

The rule for deciding the projects in case of IRR is that if:

- IRR> Discount rate, accept the project.

- IRR < Discount rate, reject the project.

After computing the IRR, it can be observed that in both stores IRR is greater than the discount rates and even though NPV of Store 1 is greater than Store 2, IRR of Store 2 is greater than Store 1. Regardless, both of the projects should be accepted but in case the company cannot afford both projects i.e. they are mutually exclusive, a store with higher NPV will be chosen as it maximises shareholders’ wealth. This is common occurrence when it comes to capital budgeting for multinational corporations.

The limitations of IRR are:

- It doesn’t give you dollar value and only provides percentages.

- It doesn’t account for non-linear cash flows, i.e. net cash flows can be negative sometime.

- Payback Period and Discounted Payback Period

Payback Period Method is one of the traditional methods of capital budgeting. This method evaluates the exact amount of time required for the company to recover its initial investment. In terms of formula Payback Period can be represented as:

Payback Period = Investment/ Constant annual cash flow

For example, an investment of Rs. 50,000 in a plant is expected to produce cash flows of Rs.10,000 for 10 years,

Payback Period = 50000/10000= 5 years

# Shorter the duration, the better it is considered for the investment.

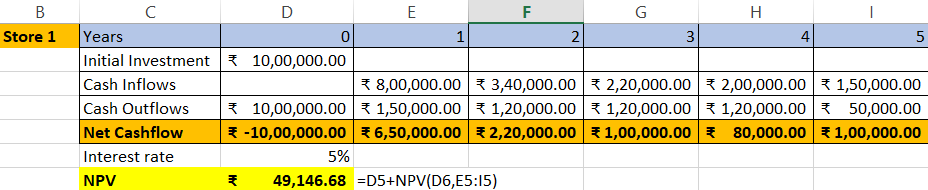

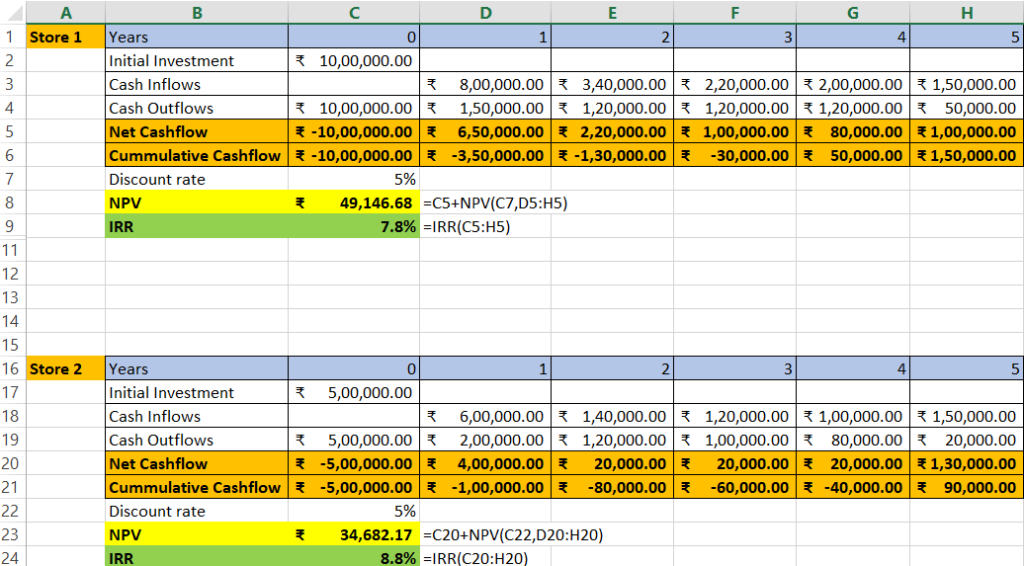

In Excel, we will first calculate cumulative cash flows. Using that we can figure out after how many years cash flows start turning positive as the payback period would be some time after the last negative cash flow. In case of Store 1, cumulative cash flows turned positive after year 3 so we use the formula:

3+ ABS(Year 3 Cumulative Cash Flow/Net Cash Flow of Year 4)

# ABS function helps us to find out the payback fraction.

Couple of drawbacks of this method are:

- It does not account for time value of money

- Only consider time and not other factors like profits.

An alternative to this method is the Discounted Payback Period which considers the effect of time value. In this method, you just have to discount the Net Cash Flows and then continue to follow the process done in the Payback Period method.

Using all these measures, we would be able to allocate our funds accordingly. In case we are required to only choose one of the two stores, we would pick Store 1 which has a higher NPV.

Last Notes – Capital Budgeting Practices in India

Capital Budgeting is widely used by the firms through multiple criteria of DCF and traditional methods. IRR and NPV are the most frequently used by private sectors, whereas Payback Period is mostly used by public sector companies. Capital budgeting decisions are taken by top management and are planned in advance. However, in some corporations investment proposals originated from plant level too. In recent times, with highly competitive markets, planning and budgeting has been a difficult task to perform. Unpredictable future cash flows, resulting from the increased volatility and competition seem to be major factors in capital budgeting decisions.

The WallStreet School’s flagship program on Financial Modelling and Valuations covers extensive practical training on topics like capital budgeting and much more in detail. It provides you with real world Capital budgeting case studies, emerging trends in capital budgeting, discussions led by industry experts and intensive training to speed up your career progression besides providing placements in Equity research, Corporate Finance, Consulting and Investment Banking domains.

If you are looking for a solid capital budgeting course or a financial modelling program, the Financial Modelling and Valuations program is the right fit for you. You will learn about essential topics such as investment analysis and decision-making, financial project evaluation, cash flow modelling, discounted cash flow techniques, NPV and IRR analysis, risk management in capital budgeting, strategic investment planning and all the important topics you will need to become a professional in financial modelling and capital budgeting.