If you are a finance professional or manager who wants to understand how strategic decisions are made inside organisations, this guide is for you.

This article explains strategic decision-making models and shows how they are applied in practice, aligned with CIMA Strategy 2026, decision theory accounting, and real management accounting tips.

First, let us clear something important.

What CIMA Strategy 2026 Means and Why It Matters?

- CIMA Strategy 2026 is not a separate paper.

It reflects how CIMA expects candidates to think when making strategic and financial decisions. - Key topics are tested through broader frameworks.

Pricing, investment, and risk appear within Financial Strategy F3, performance management, and integrated case studies. - This mirrors real business decision-making.

Finance, risk, and strategy are always connected, not handled in isolation. - Uncertainty makes this approach essential in 2026.

Changing costs, demand shifts, and technology increase the need for sound judgment. - CIMA focuses on decision quality, not just calculations.

Candidates must show structured thinking, risk awareness, and long-term value focus. - Decision theory accounting and practical management accounting tips support better choices.

They reduce guesswork and align decisions with real business outcomes.

What Are Strategic Decision-Making Models?

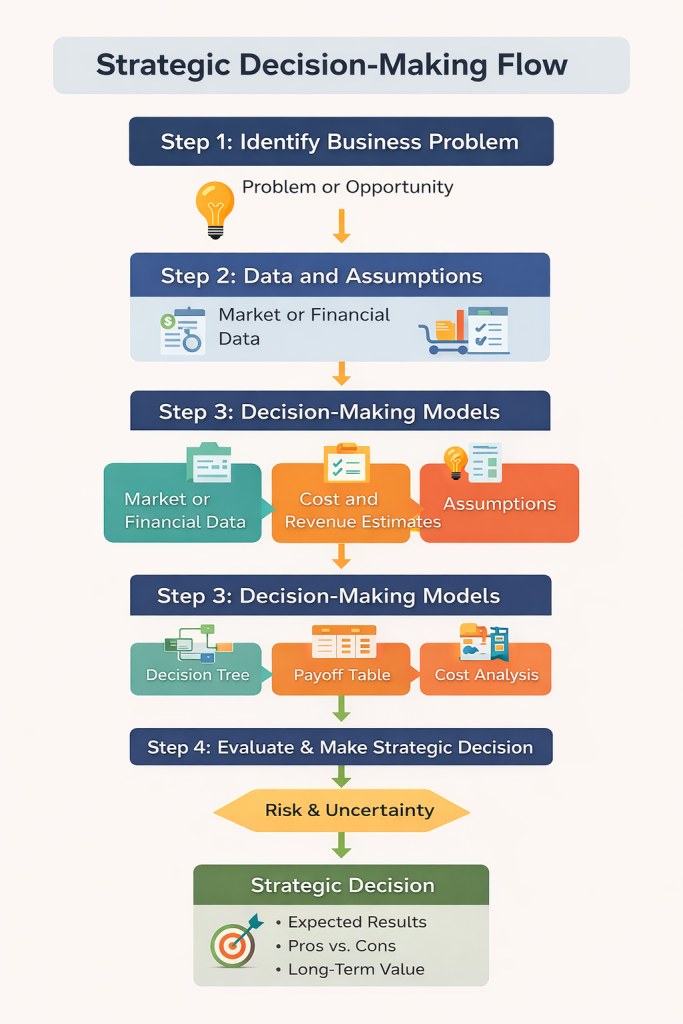

Strategic decision-making models are structured tools that help managers choose between alternatives when outcomes are uncertain.

Under CIMA Strategy 2026, these models are applied within broader financial strategy and business scenarios rather than used in isolation.

They help managers:

- Compare options logically

- Quantify risk and uncertainty

- Justify decisions clearly

This approach reflects how strategic decisions are made in real organisations, where clarity, structure, and accountability matter.

Figure 1: Strategic decision-making model used in CIMA Strategy 2026 showing problem identification, data inputs, decision models, risk assessment, and strategic outcomes.

Decision Theory Accounting in CIMA Strategy 2026

Decision theory accounting is a core foundation of strategic decision-making. It combines accounting numbers with probability logic and risk thinking.

Instead of asking what is the profit is, it asks:

- What are the possible outcomes?

- How likely is each outcome?

- What is the expected result?

In CIMA Strategy 2026, decision theory accounting supports investment appraisal pricing decisions and risk analysis within Financial Strategy F3 style questions.

This shows judgment not just math skills.

Before looking at individual tools, it helps to understand that strategic decision-making models generally fall into a few broad areas. Some models help organisations decide under uncertainty, others focus on costs and contribution, some deal with limited resources, while others support long-term investment and risk management decisions. The models discussed below cover all these areas and show how different types of strategic decisions are approached in practice.

Key Strategic Decision-Making Models You Must Know

Below are the most important models you need for CIMA Strategy 2026, always applied through broader financial strategy frameworks.

1. Decision Trees

Decision trees are structured tools used to evaluate decisions that involve uncertainty. They break a decision into different possible actions and outcomes, allowing organisations to com`pare options based on both potential returns and risks.

Suppose a company is deciding whether to launch a new product. Based on past launches and market research, management estimates a profit of ₹10 lakh if demand is high and a loss of ₹4 lakh if demand is low. They believe there is a 60% chance of strong demand. A decision tree helps evaluate whether launching makes sense.

In CIMA, decision trees often appear inside:

- Investment appraisal scenarios

- Project selection questions

- Risk-based strategic decisions

Management accounting tips for decision trees:

- Keep the structure clean

- Calculate expected values carefully

- Explain why one option is preferred

2. Expected Value Analysis

Expected value analysis is one of the most tested ideas under CIMA Strategy 2026. It helps managers choose options based on probability-weighted outcomes. This approach is commonly assessed within Financial Strategy F3 investment and risk scenarios.

Imagine a business choosing between two projects. Project A can earn ₹8 lakh, but only if things go well, which management estimates at a 40% chance. Project B earns ₹4 lakh with a higher probability of 70%. Expected value analysis helps compare these options objectively.

It reflects realistic thinking about uncertainty instead of relying on perfect assumptions.

3. Payoff Tables and Risk Attitudes

Payoff tables are used to compare how different strategies perform under various future scenarios. They help organisations understand the range of possible outcomes and choose strategies that align with their risk tolerance.

Suppose a company plans to expand into a new market. If demand is strong, profits could reach ₹12 lakh. With normal demand, profits may be ₹6 lakh. If demand is weak, the company could lose ₹2 lakh. A payoff table compares how different strategies perform under each scenario.

CIMA expects candidates to understand:

- Optimistic decision making

- Risk-averse behavior

- Regret minimization

These concepts support strategic choices rather than stand-alone theory.

4. Marginal Costing for Strategic Decisions

Marginal costing is a decision-focused costing method that considers only costs and revenues that change as a result of a decision. It helps organisations evaluate whether an action improves contribution and cash flow.

It supports decisions such as:

- Accepting special orders

- Closing or continuing operations

- Short-term pricing decisions

Imagine a manufacturer receives a one-time export order for 1,000 units at ₹120 per unit. Variable costs are ₹90 per unit, based on cost records. Fixed costs are already covered. Marginal costing shows whether accepting the order adds value.

In CIMA, marginal costing is used within wider business contexts, not isolated calculations.

Management accounting tips here are simple:

- Ignore sunk costs

- Focus on future cash flows

- Look at the contribution not the total profit

5. Limiting Factor Analysis

Limiting factor analysis is used when resources such as time, labour, or capacity are limited. It helps organisations prioritise activities that generate the highest contribution from the constrained resource.

Suppose a factory has only 2,000 machine hours available this month. Product X earns a contribution of ₹50 per hour, while Product Y earns ₹30 per hour. Limiting factor analysis helps decide which product to prioritise.

This model supports operational strategy decisions under CIMA Strategy 2026 and links planning with profitability.

How Strategic Decision Making Models Are Applied in Practice

1. Strategic Pricing Decisions Within Financial Strategy

Strategic pricing is important, but under CIMA Strategy 2026, it is not tested as a separate speciality.

Instead, pricing decisions are assessed within:

- Financial Strategy F3 frameworks

- Competitive positioning scenarios

- Contribution and value analysis

Decision theory accounting helps evaluate pricing outcomes under uncertainty.

Management accounting tips for pricing:

- Do not rely only on full cost

- Understand contribution margins

- Consider long-term strategic impact

2. Strategic Investment Decisions and Capital Allocation

- Strategic investment decisions are about where a company puts its money to grow in the future.

- Capital allocation means deciding which projects, businesses, or assets deserve funding and which do not.

These decisions are central to Financial Strategy F3 and closely aligned with CIMA Strategy 2026 thinking because they shape long term value, risk exposure, and business direction.

To support these choices, companies use structured financial models such as:

- Net present value to measure long-term value creation

- Internal rate of return to compare project returns

- Discounted cash flow to account for the time value of money

- Risk-adjusted returns to reflect uncertainty

Decision theory accounting strengthens these models by adding scenario analysis and probability weighting, helping managers choose investments under uncertainty.

This approach reflects how real companies evaluate investments before committing large amounts of capital.

3. Risk and Uncertainty in Strategic Decisions

Strategic decisions are almost always made under uncertainty. Demand can change, costs can move, and external events can disrupt plans without warning. Because of this, risk is not something businesses can ignore or eliminate.

CIMA Strategy 2026 views risk as something to be understood and managed. Instead of relying on a single forecast, decision makers examine how outcomes change when key assumptions shift. This helps reveal where a strategy is fragile and where it is resilient.

By exploring different possible outcomes and weighing potential returns against uncertainty, organisations can make more balanced decisions. This approach leads to strategies that are better prepared for change, not just optimistic about the future.

4. Behavioural Aspects of Decision Making

CIMA also recognises that managers are human so their decisions are influenced by biased emotions and pressure.

CIMA Strategy 2026 encourages systems and models that reduce bias using data and structure.

Management accounting tips here include:

- Challenge assumptions

- Separate emotion from numbers

- Document reasoning clearly

Practical Management Accounting Tips for 2026

Some practical management accounting tips aligned with CIMA Strategy 2026:

- Always identify the decision being made

- Remove irrelevant information

- Focus on future outcomes

- Consider risk alongside return

- Communicate decisions simply

These tips work in exams and in real business roles.

If you want a complete walkthrough of CIMA eligibility, syllabus, fees, and career scope for 2025–2026, this video explains it clearly:

Strategic decision-making is not about perfect answers. It is about structured thinking.

CIMA Strategy 2026 equips professionals to make better decisions in uncertain environments by using logic models and financial insight. When decision theory accounting meets practical management accounting tips, finance professionals move from scorekeepers to strategic advisors.

In 2026, businesses do not need more data. They need better decisions. And that is exactly what CIMA Strategy 2026 thinking delivers.

Build CIMA-level thinking, not just exam answers, with The WallStreet School’s CIMA Coaching Classes, designed for real-world decision-making. This will help you learn how professionals actually think.

People Also Ask

1. What is CIMA Strategy 2026 in simple terms?

CIMA Strategy 2026 is a mindset that links finance, risk, and strategy to support better long-term business decisions.

2. Are strategic decisions tested as separate topics in CIMA?

Ans. No. They are assessed within broader frameworks like Financial Strategy F3 and integrated business scenarios.

3. What are strategic decision making models?

Ans. They are structured tools that help managers compare options, manage uncertainty, and make clear, defensible decisions.

4. How does decision theory accounting help in decision making?

Ans. It combines financial data with probability and risk to evaluate choices under uncertainty.

5. Why is risk important in strategic decision making?

Ans. Because uncertainty affects outcomes, understanding risk helps organisations make more resilient and balanced decisions.