Understanding the different kinds of risk that financial institutions face is one of the core parts of risk management basics. If you are preparing for the FRM (Financial Risk Manager) exam, especially the sections that cover market risk vs credit risk, this article breaks everything down in simple words so you can grasp the big ideas without getting overwhelmed.

We will talk about what each risk means, how they affect banks and investors, how professionals measure and manage them and why FRM aspirants need to know both well. By the end of this guide, you should feel confident explaining these ideas in your own words.

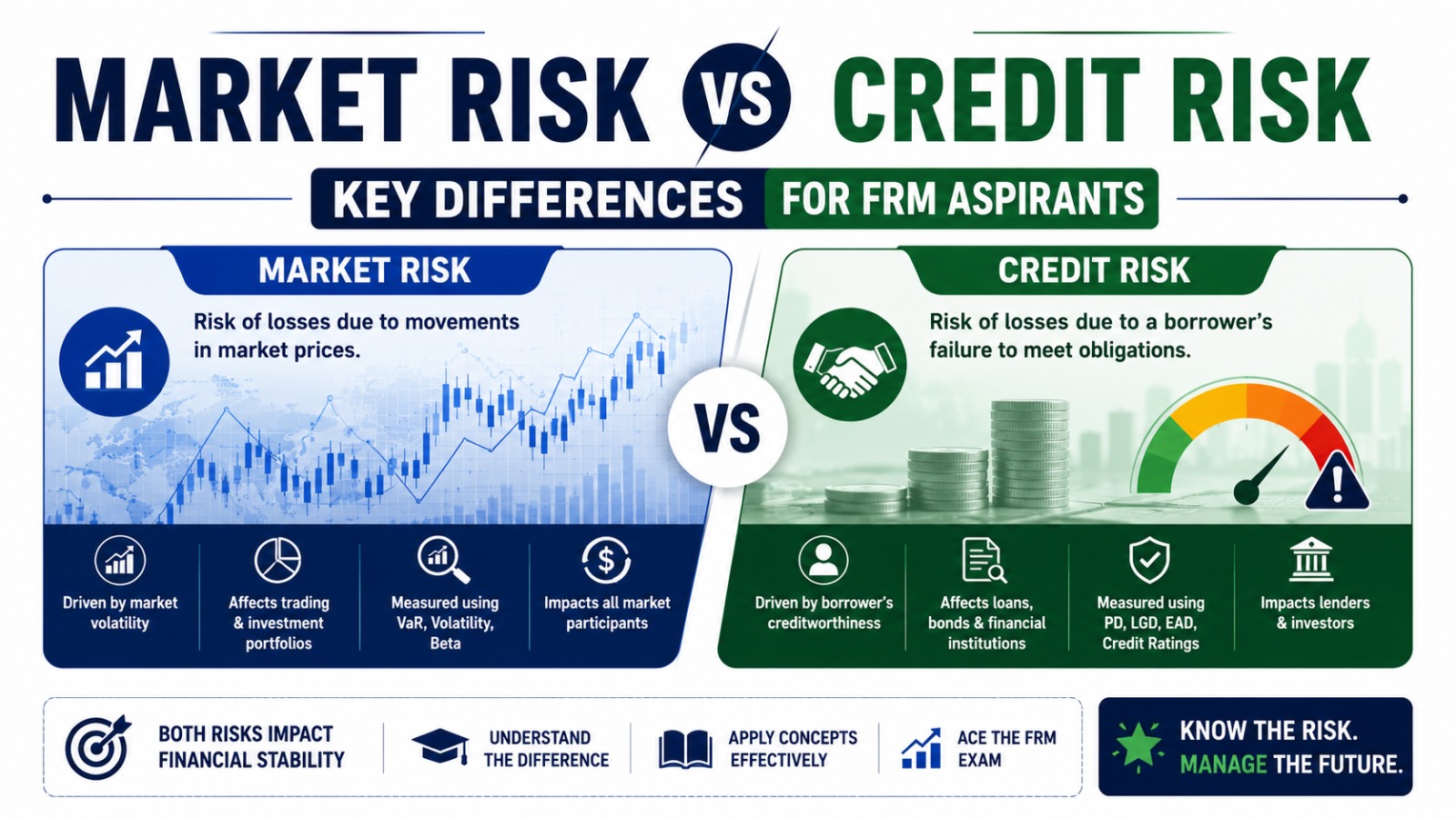

What Is Market Risk?

When we talk about market risk, we are talking about losses that come from things changing in financial markets. If prices rise or fall unpredictably, you could lose money. This happens in stocks, bonds, interest rates, currency exchanges, commodities and other asset prices.

For example:

- If the stock market drops suddenly, the value of share investments goes down.

- If interest rates rise, bond prices usually fall.

- If a company has assets priced in another currency, changes in exchange rates can affect value.

Market risk is something every investor or financial institution that owns market-linked assets must deal with. It is part of risk management basics because market movements are always happening and can never be fully ignored.

What Is Credit Risk?

Now let’s look at credit risk. This type of risk comes up when someone who owes money might not pay it back. That could be a borrower, a company or even another bank. If they default or delay payment, the lender can lose money.

In simple words, credit risk is about trust and payment. You give somebody money today with a promise that they will pay you later. If they fail to do so, that is credit risk.

Credit risk is a big deal in lending business models like banks, NBFCs (non-bank financial institutions) and lenders. Loan defaults not only reduce profits, but also weaken the capital base of the institution if many borrowers fail to pay back. This is why credit risk is a core part of FRM concepts explained for new learners.

Market Risk vs Credit Risk: Main Differences

If we compare market risk vs credit risk, the first thing you notice is that they look similar but affect financial firms in very different ways.

Here are the main points of comparison:

Figure 1: Market risk vs credit risk comparison showing key differences in source, impact, speed, and measurement for FRM aspirants.

So when you’re learning market risk vs credit risk, remember: market risk is all about movements in markets, while credit risk is about people and companies failing to pay back what they owe.

How These Risks Matter for FRM Aspirants?

If you are preparing for the FRM exam, knowing the differences clearly is not enough. You also need to understand how each risk is measured and managed in real life.

1. Market Risk Measurement

For market risk, professionals use tools like:

- Value at Risk (VaR), which shows the maximum expected loss in a given time frame with a certain confidence level.

- Stress testing to see how a portfolio would perform under extreme market moves.

- Volatility analysis to measure how much prices swing around.

Understanding these tools helps you explain why market risk is important and how traders and risk managers control it.

2. Credit Risk Measurement

Credit risk uses different methods, such as:

- Probability of Default (how likely a borrower will fail).

- Loss Given Default (how much money might be lost).

- Exposure at Default (the amount at risk when default happens).

- Credit scoring and rating systems to grade borrower risk.

These are part of FRM concepts explained when you cover credit topics. They help risk managers decide how much capital to hold and how to limit losses from defaults over time.

What Can We Learn from Real-World Cases?

History makes one thing very clear. When we compare market risk vs credit risk both behave differently, but ignoring either one can destroy even large institutions.

A well-known credit risk-driven failure was Lehman Brothers. For years, the firm kept giving poor-quality loans and took excessive credit exposure. The damage did not happen overnight. Credit risk builds slowly. The balance sheet weakens quietly. When trust finally broke, funding vanished and a long credit problem suddenly turned into a full liquidity collapse. What looked manageable for years ended in bankruptcy.

On the market risk side, Silicon Valley Bank showed how fast things can fall apart. The bank did not fail because borrowers stopped paying loans. It failed because interest rates moved sharply. Bond values dropped, depositors panicked, and withdrawals exploded. Within days, a market-driven loss turned into a liquidity crisis, even though many assets were still technically sound.

Closer to home, Yes Bank reflected a dangerous mix of both risks. Weak credit decisions led to rising bad loans over time. As trust eroded, liquidity pressure followed. Once confidence dropped, deposit outflows increased and regulators had to step in. This case clearly shows how credit risk can quietly grow and later trigger liquidity stress.

The lesson for FRM aspirants is simple and repeated across countries. Credit risk failures usually grow slowly and feel invisible until it is too late.

Market risk failures are fast, visible, and brutal.

Ignoring one type of risk just because the other looks under control is not risk management. It is professional negligence. Understanding market risk vs credit risk together is a core part of risk management basics and a key reason why FRM concepts explained focus so heavily on real-world failures not just theory.

How Risk Management Professionals Deal with These Risks?

People working in risk management do a lot of things to manage both market risk and credit risk at the same time. This is part of risk management basics that FRM aspirants must learn.

For market risk:

- Diversify the portfolio so not all assets move together.

- Use hedging strategies, like options and futures to protect against losses.

- Regularly monitor market variables.

For credit risk:

- Check credit history and scores before lending.

- Use collateral to secure loans.

- Limit exposure to risky borrowers.

Knowing these helps you explain not just what the risks are but how financial firms keep themselves safe.

If reading this helped you finally understand how market risk vs credit risk actually works in real life, that’s exactly how The WallStreet School FRM course is designed. It focuses on clear explanations, real examples, and exam-relevant thinking so you are not just memorizing concepts, but truly understanding risk the way FRM expects.

Are Market Risk and Credit Risk Connected?

Yes, they can be connected.

Sometimes changes in market prices affect borrowers’ ability to pay back loans. For instance, if interest rates jump and borrowers struggle to repay, defaults could rise. This shows how in real life, risks do not stay in separate boxes. Professionals need to understand the link between market risk vs credit risk to make better decisions today.

People Also Ask about Market Risk vs Credit Risk

1: What is the difference between credit risk and market risk?

Ans. Credit risk means borrowers may not repay money, while market risk comes from price changes in stocks, interest rates, currencies and other assets.

2: Why is market risk vs credit risk important for FRM aspirants?

Ans. FRM exams test how well you understand, measure and manage market risk vs credit risk using practical tools and real financial situations.

3: Which risk is more dangerous, market risk or credit risk?

Ans. Both matter. Market risk causes sudden losses, while credit risk builds slowly and can weaken institutions over time.

Summary for FRM Aspirants

Let’s wrap up what you should take away:

- Market risk vs credit risk are two of the main types of financial risk every risk manager must understand.

- Market risk comes from market price changes while credit risk comes from borrowers not paying back.

- Both risks are measured and managed in different ways but both are part of FRM concepts explained in the FRM syllabus.

- Knowing the tools used to measure these risks and how they are managed in real financial institutions gives you an edge in exams and in real work.

If you can explain these differences and relate them to simple examples, you are already ahead in your FRM journey.