Valuation is the process of figuring out what a company is worth today. For mature companies, this is straightforward because they have revenue history, stable cash flows and predictable performance. But startups live in uncertainty. They are still building products, still testing markets, still figuring out customer behaviour. That is why early-stage valuation is a completely different game.

Because so much is uncertain, valuation takes on more meaning than just a number. As Aswath Damodaran explains in an interview with MorningStar, “A good valuation is a bridge between stories and numbers…” The numbers are still forming, but the story around the market, the product, and the team already matters.

As for investors, it helps them to judge two things: how much risk they are taking and what kind of return they can realistically expect. And for founders, it directly affects dilution and future fundraising decisions.

Before jumping into Startup Valuation Models, let’s look at the key inputs investors review.

Table of Contents

Key Inputs Required For Any Startup Valuation

These inputs shape how investors interpret your potential and risk.

Why Traditional Valuation Models Do Not Work For Startups?

Traditional models like EBITDA multiples or asset-based valuation need stable financial data. Startups do not have that.

As Andreessen Horowitz explains in this essay “When Entry Multiples Don’t Matter”, for high-growth private companies, valuation is driven less by current numbers and more by expected future outcomes such as scale, margins, and exit potential. In other words, early-stage valuation is shaped by what a company can become, not by what it has already achieved.

This is why the early-stage companies use Startup Valuation Models instead of traditional corporate models.

Valuation Models For Startups

- Berkus Model

The Berkus Model is used when a startup is still very early and does not have real revenue yet. Instead of forcing financial projections that do not mean much at this stage, the model looks at a few basic things that create value early on.

These include the strength of the idea, the quality of the founding team, whether a prototype exists, early signs of traction, and how close the startup is to launching properly. Each of these areas adds a fixed amount of value, and when you put them together, you get a rough but reasonable valuation.

The idea behind this model is simple. It helps founders and investors avoid wild guesses and keeps early valuations within a sensible range.

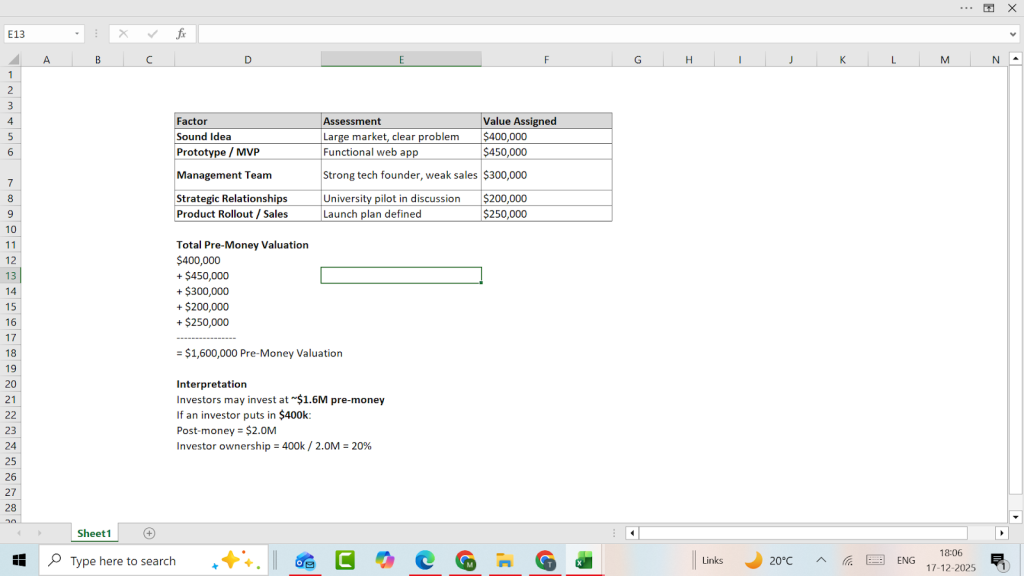

Berkus Valuation Example:

Startup: EduTech AI

Stage: Pre-revenue

Product: AI tutoring platform for college students

Assume:

- Max per factor: $500,000

- Maximum valuation: $2.5 million

Figure 1

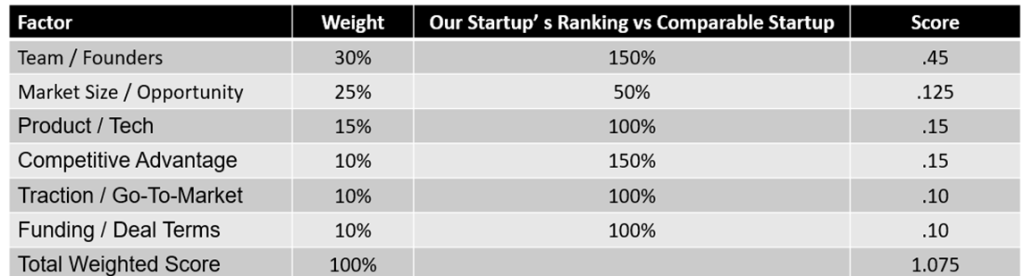

- Scorecard Method

The Scorecard Method is used for early-stage startups that lack substantial financial data yet. Instead of estimating a valuation from scratch, it starts with the average valuation of comparable funded startups. Then the target startup is compared against these benchmarks across key factors such as the founding team, market size and opportunity, product and technology, competitive advantage, traction, and go-to-market strategy. Based on how the startup performs on each factor, the final valuation is adjusted up or down against the benchmark.

The idea is to keep valuation realistic by comparing the startup with others like it, rather than relying only on hope or projections.

Figure 2

Comparable Startup Pre-Money Valuation: USD 100 mn

Implied Value of our Startup: 100 x 1.075 = USD 107.5mn

- Venture Capital (VC) Method

The VC Method looks at the startup from the investor’s point of view. It does not focus on what the company is making today.

Instead, it asks what the company could be worth in the future if everything goes well.

From that future value, investors work backwards based on the return they want. This helps decide what the startup should be worth today, even when there is no profit or steady revenue yet.

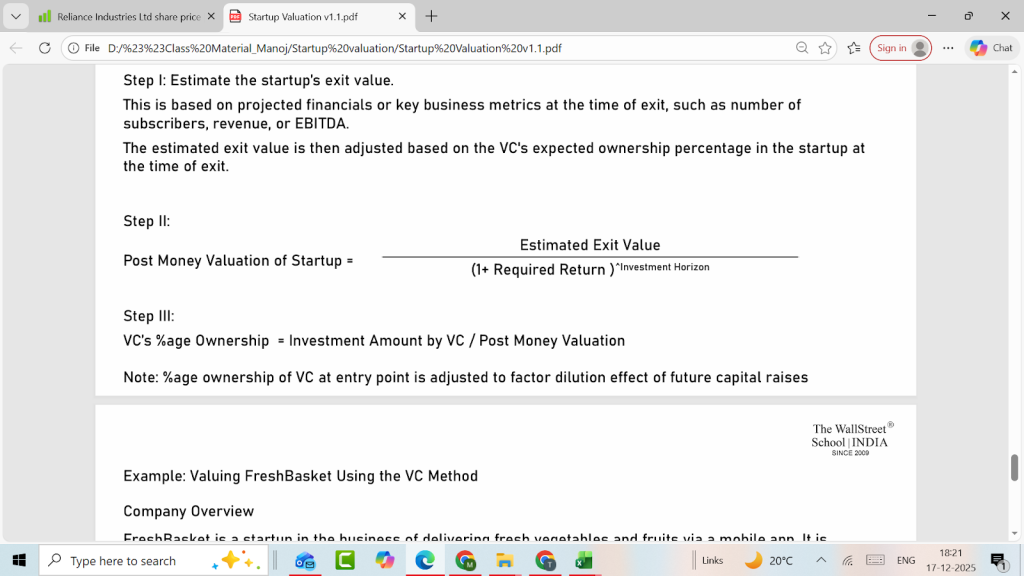

Step I: Estimate the startup’s exit value. This is based on projected financials or key business metrics at the time of exit, such as the number of subscribers, revenue, or EBITDA. The estimated exit value is then adjusted based on the VC’s expected ownership percentage in the startup at the time of exit

Step II:

Figure 3

Step III:

VC’s %age Ownership = Investment Amount by VC / Post Money Valuation

Note: %age ownership of VC at the entry point is adjusted to factor in the dilution effect of future capital raise

- DCF (Discounted Cash Flow)

The DCF method values a startup based on the cash it is expected to generate in the future. Those future cash flows are then adjusted to reflect risk and the fact that money in the future is worth less than money today.

While this method comes from traditional finance, it can work for startups once there is some visibility on revenue and cash flows. As EY Netherlands explains, “The main advantage of the DCF method is that it values a firm on the basis of future performance. In other words, it is perfect for a startup that might not really have realized any historical performance yet.”

- Comparable Company Analysis

Comparable Company Analysis values a startup by looking at how similar companies are valued in the market. These companies could be public or privately funded.

There are two main ways to do this.

- Trading comps look at public companies and their valuation multiples to get a sense of market pricing.

- Transaction comps look at recent funding rounds or acquisitions of similar startups, which often feel more relevant for early-stage companies.

The idea is to find businesses with similar models, growth patterns, and markets, and then apply similar valuation multiples.

This approach is helpful because it grounds valuation in real market behaviour. Instead of asking what a startup should be worth in theory, it looks at what investors are actually paying for similar businesses.

- Cost to Duplicate (Asset-Based / Build-Cost Approach)

The Cost-to-Duplicate Method asks a very basic question: How much would it cost to build this startup again from scratch? It adds up expenses like product development, technology, hiring, and infrastructure. The result gives a baseline value based on what has already been invested.

This method does not capture future growth or potential, but it can be useful as a lower bound, especially for technology-focused startups where a lot of effort has already gone into building the product.

How do founders and investors make a decision on which model to use?

This decision usually follows a simple logic. They don’t start by picking a valuation formula. They first try to understand the business step by step.

Step 1: Look at the stage of the company.

The first thing people check is the stage. Is the startup already making money, or is it still building traction? This matters because the stage decides what kind of valuation even makes sense. A company with no earnings cannot be valued the same way as one that has started showing steady revenue.

- If a startup has started generating revenue or has some visibility on future cash flows, then a DCF model can be used. DCF focuses on future performance rather than past numbers.

Step 2: Look at the nature of the business.

Once the stage is clear, the next question is what kind of business this is. For example, a SaaS company creates regular, repeat data, behaves very differently from marketplaces that depend on activity and volume. On the very other hand, AI startups usually take longer to build, while consumer apps move faster but see more user drop-off. Because different business models produce different types of data, and that influences which valuation method fits.

- When there are enough similar startups that have already raised funding in the same space, market-based methods start to work well. Trading comps, Transaction comps and the Scorecard Method make sense here because they compare your startup with similar startups that have already raised funding and adjust the valuation based on how strong your team, market, product, and traction are compared to them.

- Cost-to-Duplicate method can also be used here as a simple reality check. If a startup has spent real time and money building the product or tech but hasn’t made much revenue yet, this method helps show the minimum value by asking one basic question: What would it cost to build this again from scratch?

Step 3: Look at how strong the data really is.

The final check is the quality of the numbers available. If the financial projections depend on too many assumptions, or if there is no revenue history at all, then detailed cash-flow models stop being useful.

- In these situations, the VC Method usually works better. Instead of focusing on current earnings, it looks at what the company could be worth at exit and what return the investor wants.

So the rule is simple:

Practical Valuation Workflow

Here are practical steps that can be followed. Clear and simple.

Step 1: Get the basics clear

Start with the obvious stuff. Who’s on the team? How far along is the product? How big is the market? What kind of traction do you have so far? These basics shape every Startup Valuation Model you’ll use later.

Step 2: Sketch simple financial projections

Put together rough numbers for the next three years. Don’t try to make them perfect. Investors know projections are guesses. What they care about is whether your assumptions sound reasonable and whether you understand how the business could grow.

Step 3: Try more than one valuation method

Don’t depend on a single model. Use two or three that fit your stage. Maybe Scorecard or VC Method, and DCF if you already have some revenue. Each method will point to a slightly different number, and that’s completely normal.

Step 4: Turn those numbers into a range

Lay all the results next to each other. The lowest and highest numbers give you a valuation range. Investors usually prefer this because it shows you’re flexible and not stuck on one figure.

Step 5: Sense-check it for your industry

Every sector behaves differently. SaaS companies often get higher multiples. Deep-tech or hardware startups usually take longer to scale. Adjust your range a bit based on what’s normal in your space.

Step 6: Be ready to explain your thinking

Investors care less about the final number and more about how you got there. If you can clearly explain your assumptions and logic, your valuation automatically feels more believable.

Step 7: Pressure-test your valuation

Ask yourself what happens if growth is slower or costs are higher than planned. If the number still feels fair, you’re probably in a good place.

Common Mistakes in Startup Valuation

- Assuming everything will go right and growth will be much faster than reality

- Quoting a huge market size without knowing how much you can actually reach

- Comparing yourself with the wrong companies or copying their pricing blindly

- Not being clear on how your own business really makes money

Conclusion

Valuation works best when you treat it as a thinking exercise, not a math trick. There is no single right number, and the right approach always depends on your stage, your business model, and the quality of data you have. Using more than one model helps you arrive at a realistic range, and investors usually care more about how you explain your assumptions than the final valuation itself. When your logic is clear, the number automatically feels more credible.If all these valuation models made you think, “Wow, I need to learn this properly”, The WallStreet School’s Financial Modelling and Valuations Course is the perfect next step.

The concept that valuation is a ‘bridge between stories and numbers’ really resonates. I think this is especially crucial when dealing with early-stage startups, where the numbers can be so uncertain, but the vision can still be clear.